Investment Insights

Scott Hoxer serves as Chief Investment Officer for Alliance Wealth Advisors, writing about investment insights and providing market commentary.

By Scott Hoxer

Economics, Elections, and Geopolitics

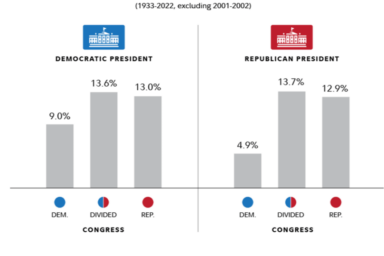

Markets are complicated systems driven by almost innumerable variables, but generally speaking, ...

By Scott Hoxer

Investment Insights Winter 2023

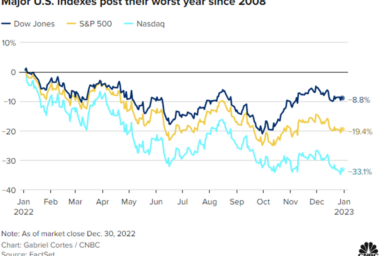

Rebound year? 2022 was a particularly challenging year for markets and one ...

By Scott Hoxer

Investment Insights Summer 2023

Summer Heat For large swathes of the United States, the summer of ...

Download ebook

Our guides have been designed to give answers to all of the difficult questions surrounding retirement.

By Scott Hoxer

Investment Insights Spring 2023

Fact or Fiction? 2023 has been mixed in terms of economic data ...

By Scott Hoxer

Investment Insights August 2022

What Does Autumn Hold? Every year as we enter the end of ...

By Scott Hoxer

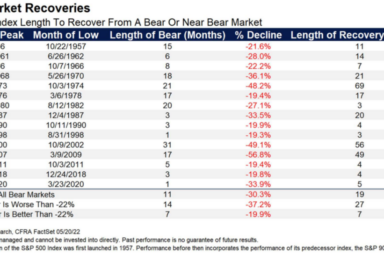

Investment Insights June 2022

Anatomy of a Bear Market As of the time of this writing ...

By Scott Hoxer

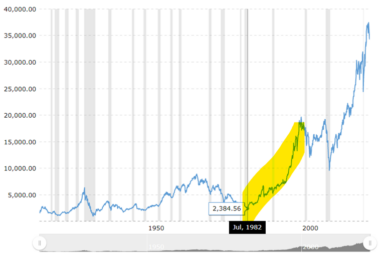

Investment Insights April 2022

Reasons for Optimism For many months running, the headlines in popular press ...

By Scott Hoxer

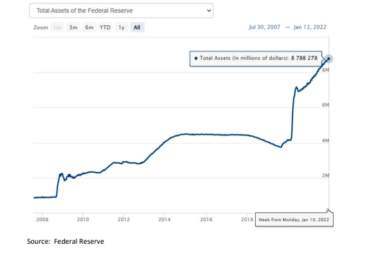

Investment Insights February 2022

2022 Outlook 2022 has dawned with heightened volatility and concerns that a ...

By Scott Hoxer

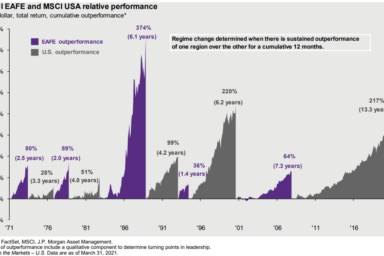

Investment Insights April 2021

International Markets Amidst the events of the past year, much investor focus ...

By Scott Hoxer

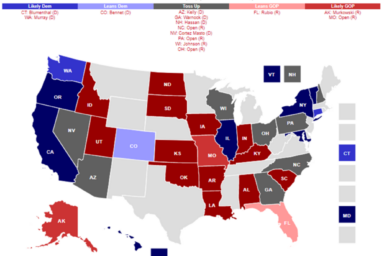

December 2020 Investment Insights

As the dust has somewhat settled on a chaotic and contentious election ...

By Scott Hoxer

September 2020 Investment Insights

It has become cliché to talk about 2020 as a historic and ...

By Scott Hoxer

February 2020 Investment Insights

Of Bitcoin and Bubbles As 2021 has begun, markets and asset prices ...