International Markets

Amidst the events of the past year, much investor focus has centered around US markets and the US economy. Often lost in this discussion is how international markets have fared and what the outlook is for international markets. International markets can comprise a part of a well-diversified portfolio and for this month’s Insights, I thought it would be helpful to provide a bit of a primer and commentary around investing internationally via a Q&A format.

Why Should I Consider International Holdings in My Portfolio?

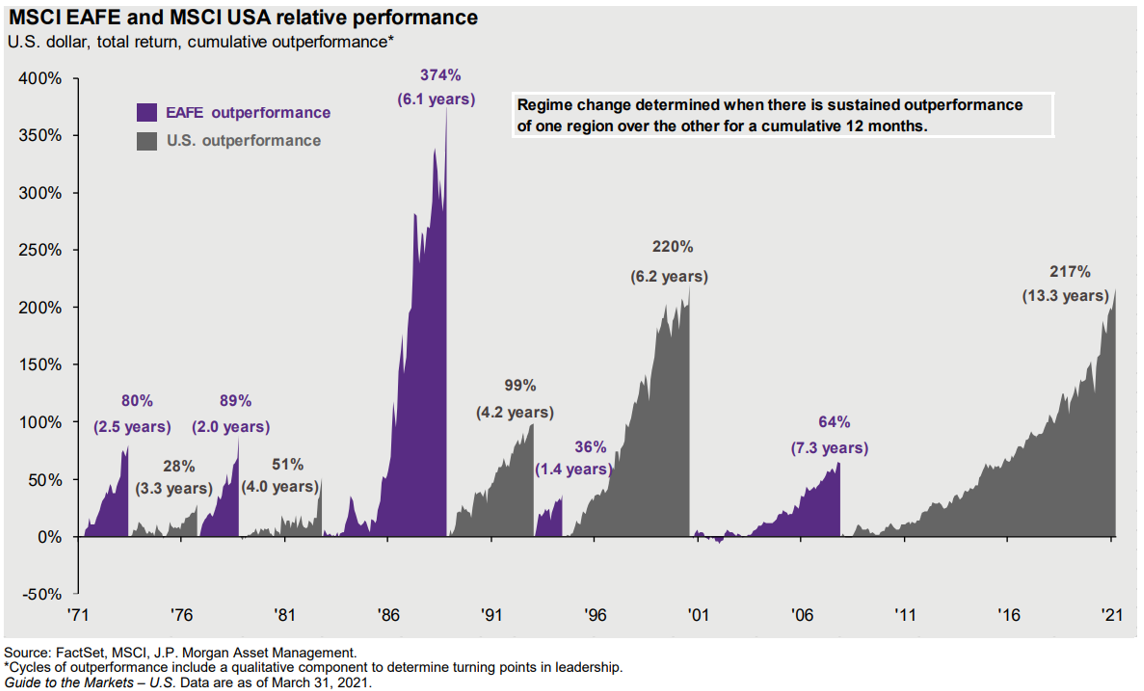

Because none of us have a crystal ball, we spread our portfolio across a variety of assets, some of which should be non-correlated. By having non-correlated assets, we provide some ballast to our portfolios during different market conditions. The challenge with diversification is to not be over diversified. Over diversification can significantly dilute performance and my experience is that many investors over diversify their portfolios. That being said, a diversified portfolio is key to successful investing and international holdings can play a key role in reducing overall portfolio risk via non-correlation. Consider the below chart of international performance (purple) compared to US performance (grey):

Here we observe changing market leadership over time. There are periods of time where US markets outperform and other periods of time where international markets carry the day. I recall the 2000s where international markets consistently outperformed US markets. US markets have since significantly outperformed, but if history is any indicator, we’ll see periods of time in the future where international has its day.

Is International Investing Risky?

As with any investment, investing internationally carries risk. International investments will fluctuate in value. Not all international investing, however, carries the same amount of risk. International markets are often delineated between developed and emerging markets. Developed markets are established, mature economies (think Canada, Germany, the UK, etc.) and many of the established multinational companies domiciled in these countries carry similar risk to established US multinational companies. In contrast, emerging markets are developing economies (i.e. Indonesia, Thailand, Ghana, etc.) that often exhibit high returns, but carry a high degree of risk.

What are Some Common International Strategies?

The international strategies we use in client portfolios have two different approaches. One is a fundamental, bottom-up approach where investment selection committees perform a thorough analysis of individual companies. They look at financial statements, interview management, look at industry factors and typically hold investments for a long period of time. A contrasting strategy is a relative strength or momentum-based strategy where investments are made in companies have been doing well relative to another investment. The idea here is to identify a hot hand and continue to ride the momentum. Both strategies have fared well although the approaches are very different in nature.

How has International Fared in Recent Years?

International markets have significantly lagged US markets in recent years. An investor in US markets (purple) would have outpaced an international investor (blue) by over 173 percentage points over the past 10 years:

Source Yahoo Finance

$100,000 invested in US markets over this time period would have grown to nearly $300,000 while $100,000 in international stocks would have only grown to a little over $122,000.

What is the Outlook for International in the Coming Years?

Anytime we see spreads to this degree, we question the durability of spread and the likelihood of mean reversion (things going back to normal). International valuations represent a very substantial value relative to US markets and the odds seem likely that the gap will narrow at some point. The difficulty, however, lies in the following:

-When we see historical price deviations, we still don’t know when the mean reversion will occur. Timing market pivots correctly is extremely difficult

-Perhaps a high degree of the US price premium is due to investors perceiving higher US earnings “quality”, meaning there is a perception that US earnings are more predictable or more stable or that the growth prospects for US companies are better

-When crises occur, the US is often perceived by investors as the least bad option and it seems that there is some sort of price premium assigned as a result

Even considering above, the value is compelling enough that international markets should be considered. Moreover, as international markets are trading at relatively low levels, the price declines are potentially less than US markets (since valuations are already relatively low).

International markets often draw some concern from US investors and perhaps some of that is warranted given the past 10 years, but we feel that for many investors international investments should comprise a part of their portfolio. The value is compelling and the added layer of diversification can be of benefit during uncertain times. As always, these comments are intended to be general in nature and the application to your specific situation should be reviewed with your financial advisor prior to implementing any changes.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

Diversification, asset allocation and rebalancing strategies do not ensure a profit and do not protect against losses in declining markets. Rebalancing may cause investors to incur transaction costs and, when rebalancing a non-retirement account, taxable events may be created that may affect your tax liability.

Investing involves risk, including loss of principal. Supporting documentation for any claims or statistical information is available upon request.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve. Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Registered Investment Advisors with and advisory services are offered through Alliance Wealth Advisors, LLC, an SEC Registered Investment Advisor. The firm only transacts business in states where it is properly registered, or is excluded or exempted from registration requirements. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the advisor has attained a particular level of skill or ability. Alliance Wealth Advisors is not affiliated with any other named entity.