Retirement GPS

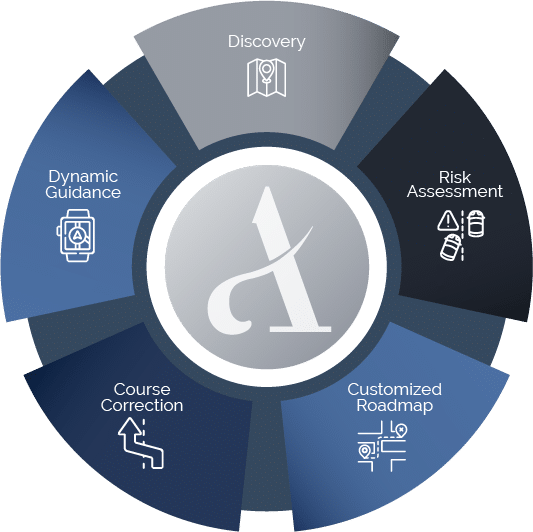

Discovery

The first thing a GPS needs is information. Where do you want to go? How much fuel do you have? How fast do you like to drive? Do you prefer freeways, city streets or scenic highways?

Risk Assessment

A GPS can triangulate precisely where you are now in relation to your goals & warn you about dangers you can’t see: road construction, speed limits, traffic conditions, and accidents. Its Important to know your blind spots.

Customized Roadmap

A GPS is much more than just a map. It has the tools to calculate multiple route options, and identify the optimal course, customized to your unique objectives & preferences.

Course Correction

You may need to make a few lane changes to get on the optimal route. A GPS assists in making necessary adjustments to get you on the right track.

Dynamic Guidance

If goals or conditions change the GPS recalculates your route staying with you every mile to ensure you get to your destination safely and efficiently.

The Market Minute

Watch our past Market Minutes for insights on financial headlines, market updates, geopolitics, and retirement best practices

Investment Insights

Timely insight on the market’s and economy’s

impact on your retirement.

Retirement Resources

Explore a wide range of books and gain insights into making informed decisions for a fulfilling retirement.

The AWA Impact

0

Fiduciary Advisors0

Employees0+

Households$0+

Assets ManagedHave A Question?

Reach out here.

General Resources

There are thousands of licensed advisors in our industry. With so many advisors and conflicting opinions on wealth management, it may feel overwhelming to know whose advice you can trust. One suggestion we have is to reference these regulatory agencies and accreditation sites to do a little research on your advisors.